Travel+Leisure (TNL): Is This Timeshare Stock A Buy After Dip?

Thomas Barwick/DigitalVision by way of Getty Photographs

Vacation + Leisure Co. (NYSE:TNL) has been dealing with challenges in excess of the previous couple of several years, owing to COVID-19 pandemic and unstable desire dynamics in the hospitality sector. As the economic climate reopened so too did Travel + Leisure’s business but items look established to stall yet again. Investing in timeshare companies at the beginning of a new business cycle can often give chances for important returns. Timeshares are a remarkably cyclical field so it will work both of those strategies. In downturns, luxurious big-ticket merchandise like timeshares get strike the hardest but the rebrand to Travel + Leisure gave Wyndham Places a several new resources to aid the enterprise cope during tough occasions like these. Now we are heading to acquire a glance at some of the most current resources and see how they could be benefiting buyers in the around future.

The Products

Journey + Leisure is still a timeshare corporation, but their exclusive get on the item differentiates them. As a substitute of a regular timeshare, Journey + Leisure sells trip clubs. Associates can layout their own holidays and they can use their possession in a variety of methods. It was the Iphone minute for Vacation + Leisure. They also nonetheless get routine maintenance charges for their timeshare choices which is a beneficial form of passive profits. This permitted the company to focus on creating a robust portfolio rather of buying and endorsing one particular pick spot at a time.

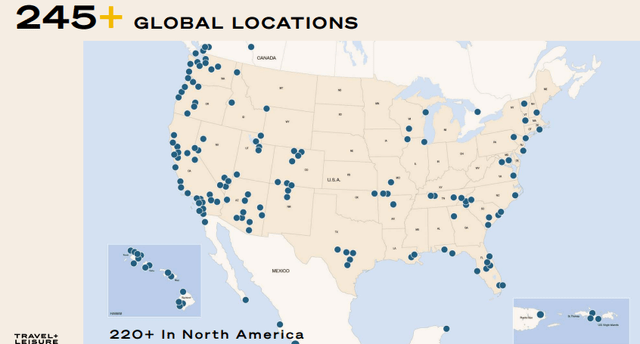

Possessing a solid lodge portfolio is pricey and makes a big barrier to entry for opponents as they have to go up from an entire fleet of inns compared to just 1 desirable spot and the TNL portfolio boasts some 245 areas in some of the most beautiful spots.

Journey + Leisure

As a result, the worth of timeshare shares relies upon largely on the range of products and destinations they offer you. Possessing a deep area catalog helps make it more challenging for levels of competition to poach shoppers and is a major selling position for new consumers. It also provides shareholders self-confidence in the company’s skill to preserve present buyers. Travel + Leisure has performed perfectly developing up its catalog.

Vacation + Leisure also has the RCI Exchange that facilitates the buying and selling of timeshare- and it can be 1 of the world’s major by quantity. They’re effectively a a single-stop store for all matters timeshare and it always appears to be associated in any ground breaking options in the place.

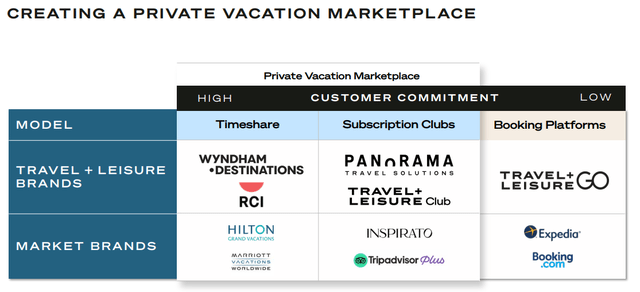

Some queries have been lifted about the timeshare industry’s potential to entice millennial revenue, but there are some endeavours underway that should assist it improve. Vacation + Leisure started presenting membership solutions to millennials who are not as probable to dedicate to a long-time period financial commitment. The introduction of Panorama’s subscription solutions could be pivotal for Travel + Leisure, specifically in light of latest opposition from Airbnb and other short-phrase lodging items. Membership services could very perfectly stop up getting the next frontier in the timeshare marketplace.

Travel + Leisure

Sturdy Gross Margins Put up Recovery

Many thanks to an enhanced price proposition relative to bigger lodge prices and strong employment figures, TNL’s future outlook is wanting promising.

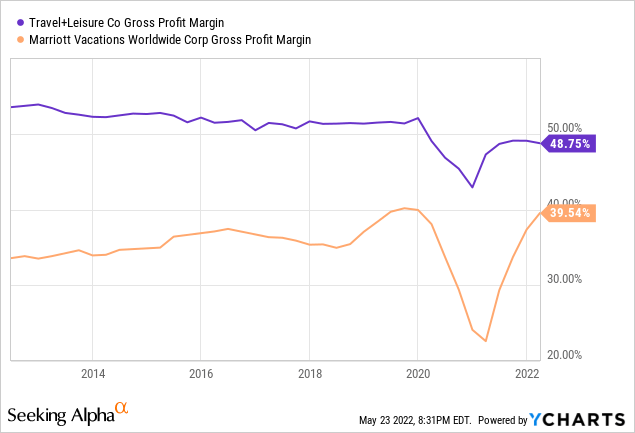

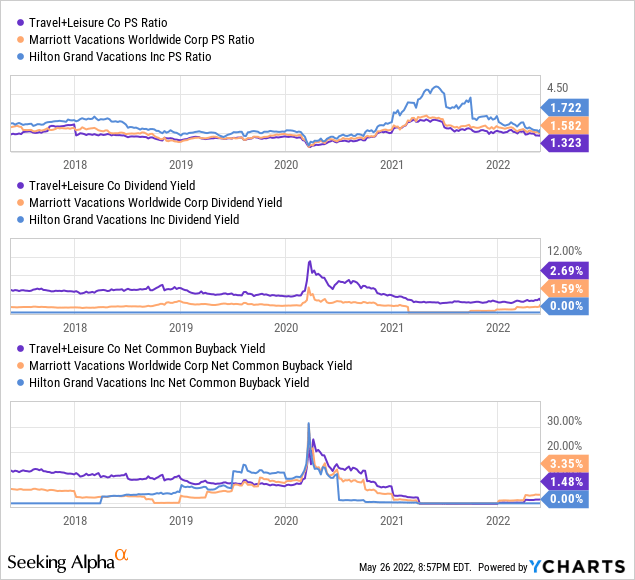

The company enjoys robust gross margins thanks to pricing energy but they have been declining. The Wyndham Locations choices exist at the medium degree of the pricing spectrum. Compared to extra lavish offerings like the Marriott Vacations clubs, you would anticipate Vacation + Leisure’s offerings to have fewer favorable margins but they truly outperform.

This is seriously a testomony to the organizational efficiency of the leadership crew. Charges have been equipped to stability out the costs, top to larger revenues. Management around maintenance agreements and a solid commission-based model allow for the organization to proficiently pass on fees to customers.

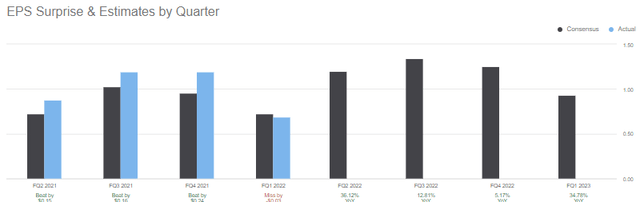

The recovery has seriously taken root for the enterprise. EPS trends have been favorable right until not too long ago. The organization has a cyclical ingredient to income and has just lately been beating estimates for the most aspect.

Seeking Alpha

Most notably in their family vacation possession business, the organization had an ordinary VPG (quantity for each visitor) of $3,377 in Q1 is bigger than ever just before for the firm and 40% earlier mentioned last year’s figures. It is also significant to try to remember that inflation is very good for their business. Costs for accommodations and trip houses are rising. This allows incorporate value to the timeshare idea for shoppers as it will become a lot more value-efficient relative to remaining in other sorts of lodging. Interest rates increasing on the other hand are additional about.

Terrible Situations for Cyclical Performs

Reviews from the Federal Reserve counsel that we are heading in the direction of rate hikes among 3-5 situations this calendar year. This will be the initial time charges have amplified considering that the start of the pandemic-induced lockdowns and it could affect financial development and equity price ranges. What is much more, there is a tendency in the timeshare industry to finance purchases so a extended period of time of bigger rates will boost the overall price of VO merchandise to the shopper.

Extended-expression traders who keep their eyes open should have a lot of alternatives if they continue to be diversified. The market place has been getting more unstable as premiums increase and issues get tenser abroad.

They affect the volatility of stocks and their multiples. When fascination costs are superior, shares are fewer desirable because they present lower returns.

The hospitality marketplace is just one of the most impacted by fascination fees simply because providers have a tendency to have a substantial debt-to-fairness ratio.

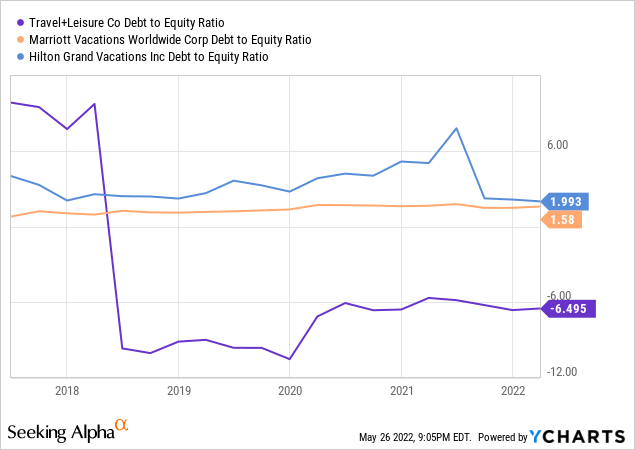

This suggests that when desire premiums go up, so does the price tag of borrowing income for these businesses. This puts timeshare companies in a rough place. They have to pay out extra to borrow cash due to the fact of the desire costs. They are likely to stay clear of this by building relatively secure agreements with fixed rates for revolving strains of credit history. This is wherever Vacation + Leisure stands out from its friends. They have nearly no personal debt and no urgent have to have for liquidity injections. It is probable that they might protected credit score to beef up the stability sheet if the economic system was to go south in a big way but the organization has accomplished these kinds of a great career running its liquidity and all round price of money that this sort of a shift really should be promptly forgiven if it were to transpire.

There is also the point that a economic downturn is not all doom and gloom for larger sized knowledge gamers like Travel + Leisure. There is normally room for crucial acquisitions at beneficial rates and Wyndham has completed some remarkable specials in the earlier. Vacation + Leisure is an outgrowth of the Wyndham brand name but it will be appealing to see if they can have identical good results in the event of a downturn.

Conclusion

Journey + Leisure is quite valued proper now. We could be going into a significant slowdown and they contact hospitality a cyclical engage in for a motive. I am by no means likely to suggest shopping for a timeshare inventory on the cusp of a recession but there is a good deal to like about Journey + Leisure below. The stock has sold off a large amount but it could even now go reduced. I would not be in a rush to acquire just nevertheless but I see no cause why buyers need to rush to section with their shares at this level. I fee the stock as a Keep.